As Middle East tensions remain in focus, the market is asking a bigger question than whether oil prices move higher in the short term. The real question is what a sustained rise in energy prices would mean for the global economy and how should one tackle the current markets.

So far, markets are reacting to the inflationary implications of higher oil rather than pricing in a full-scale economic shock. That distinction matters. A higher oil price tends to feed directly into headline inflation, even if core inflation is less affected at the start. As energy costs rise, businesses face higher transport and production expenses, which can eventually filter through into prices more broadly.

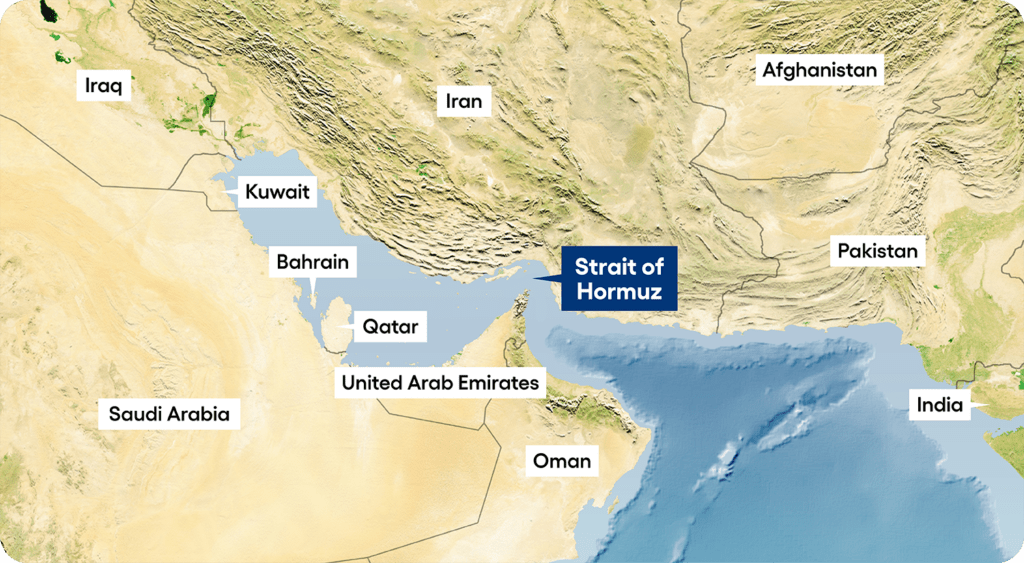

Why the Strait of Hormuz matters

The significance of the region comes down to energy flows. Around one in five barrels consumed globally passes through the Strait of Hormuz, while more than 80% of gas and oil is directed to emerging markets including India and China. This makes it one of the most important chokepoints in the world economy. When tensions rise in that area, oil markets tend to price in disruption risk quickly, even before any major supply loss is confirmed.

That helps explain why oil has moved higher, but not yet to extreme levels. Markets know there is geopolitical risk, but they also know that the supply backdrop is not the same as it was in previous decades.

The deeper point on inflation and growth

What the market is increasingly pricing is a classic cost-push shock. Higher energy prices raise input costs. Those higher costs can feed into consumer prices, that is inflation, in a period where market expectations were more aligned to interest rate cuts in the U.S. At the same time, they can weaken demand and slow activity by reducing purchasing power and putting pressure on company margins, and eventually to the global economy in general.

This is where the real risk lies. It is not only the initial move in oil. It is the duration of the conflict. If tensions persist and energy prices stay elevated, the drag on growth becomes more meaningful.

A prolonged period of conflict, a higher level of energy prices

There are reasons the market has not moved into outright panic in the initial days of the conflict. Before the latest escalation, oil fundamentals were already leaning toward relative supply comfort. OPEC+ also announced another increase in output, adding 206,000 barrels per day from April. That does not eliminate geopolitical risk, but it does provide some offset.

There is also a structural point worth remembering. Global markets are still exposed to the Middle East, but less so than in the past. The United States has become a much larger producer, with output reaching close to 14 million barrels per day in 2025. More broadly, global dependency on oil is lower than it was decades ago, even if energy still matters enormously at the margin.

We view a prolonged period of conflict as a negative driver for the global economy. However, the magnitude of the impact will be different from a regional point of view. Selective countries will suffer economically more than others.

What markets are really telling us

The regional market reaction has also been revealing. European equities came under pressure, while US equities were relatively more resilient. That suggests investors may still see the US market as a comparatively safer harbour in periods of geopolitical stress, probably given the less dependency today.

Interesting also to highlight is the fact that the US dollar is behaving as it should in periods of risk-off modes. Following a very bad year in 2025, the US dollar has regained its dominance as a safe haven currency.

Technology has also remained a pretty nuanced area. It has been among the most volatile sectors in 2026 on fear that the heavy capital expenditure in AI by the mega-caps will fail to monetise as expected, while developments by Anthropic in its offerings will pressure many existing models. However, over the past days we have seen the tech sector more resilient as investors reverted to solid fundamental names.

Why it matters

The message for investors is not to ignore the risks, but also not to confuse volatility with permanent damage. Markets are adjusting to a higher geopolitical risk premium, but the macro-outcome will depend heavily on how long the disruption lasts and whether supply tightens in a meaningful way.

A legitimate question among opportunistic investors is whether the current geopolitical turmoil poses an investment opportunity in oil. One lesson learnt from Donald Trump’s previous presidency, now being revisited in his second term, is the degree of policy unpredictability. Such unpredictability can quickly shift the outlook for energy markets, sometimes triggered by something as simple as a tweet and push energy prices lower. Indeed, we have already seen a policy reversal from Trump, with sanctions eased to allow India to purchase Russian oil that had been stranded at sea. While this move has so far failed to ease elevated energy prices, we cannot rule out further measures that could limit additional upside. Positioning in energy might carry a heightened degree of policy risk. As we have seen with the AI theme, we are also now seeing some crowded investment in energy prices. This becomes a risky proposition given the speeds and frequency with which policy and geopolitical news can alter the outlook for prices.

However, this does not mean that investors should remain on the sidelines. Instead, they should revisit companies that have recently been hit hard by AI-related fears but have shown resilience during the current market turmoil. Select technology stocks such as Microsoft and Alphabet, as well as other names like Spotify and CrowdStrike in the U.S., and Deutsche Telekom and Prosus in Europe, could present attractive entry opportunities in the current volatile market environment.

This information is issued by Calamatta Cuschieri Investment Services Ltd (“CCIS”) of Ewropa Business Centre, Triq Dun Karm, Birkirkara BKR 9034, Malta (C13729). CCIS is licensed to conduct Investment Services under the Investment Services Act in Malta by the Malta Financial Services Authority. The value of the investment may go down as well as up and may be affected by changes in currency. Any performance figures quoted refer to the past and past performance is not a guarantee of future performance nor a reliable guide to future performance. This information is being provided solely for information purposes and should not be deemed or construed as investment advice, advice concerning particular investments, advice concerning investment decisions, tax, legal, or any other ancillary regulatory advice. There is no guarantee that any forecast or opinion will be realized. The information presented does not take into account your personal circumstances and is provided to You on the express basis that it is not advice, and you may not rely upon it in making any investment decision. Investments in any financial instruments involve risks, you should make your own research before making any investment decisions and should seek the assistance of a financial advisor if in doubt. No person should act upon any opinion and/or information in this document without first obtaining professional advice. CCIS does not accept liability for actions, proceedings, costs, demands, expenses, damages, and losses suffered by persons as a result of information, views, or opinions appearing on this document.